Florida Loan Agreement [Free Printable, Fillable PDF]

A Florida loan agreement between private parties looks straightforward until you factor in Florida’s usury law, and the consequence of getting it wrong isn’t just losing the excess interest — it can mean losing every dollar you lent. Under F.S. §687.03, the maximum interest rate on a private loan under $500,000 is 18% per year, but what most private lenders don’t know is that origination fees, late fees, and extension fees that don’t reflect an actual cost to the lender count as interest under Florida law and get added to the stated rate when a court determines whether the loan agreement florida template they used crossed the legal line.

I’ve worked with private lenders who charged a modest rate and added a flat origination fee that seemed reasonable, not realizing that fee pushed their effective rate past the criminal usury threshold under F.S. §687.071 — and at that point the court doesn’t just reduce the interest, it can void the lender’s right to collect the principal entirely. The personal loan agreement florida template below is built around Florida’s usury thresholds so the rate, the fees, and the terms stay on the right side of a line that carries consequences most private lenders never see coming.

Candice Hayden, Legal Writer

Carly Johansson, Florida Contract Attorney

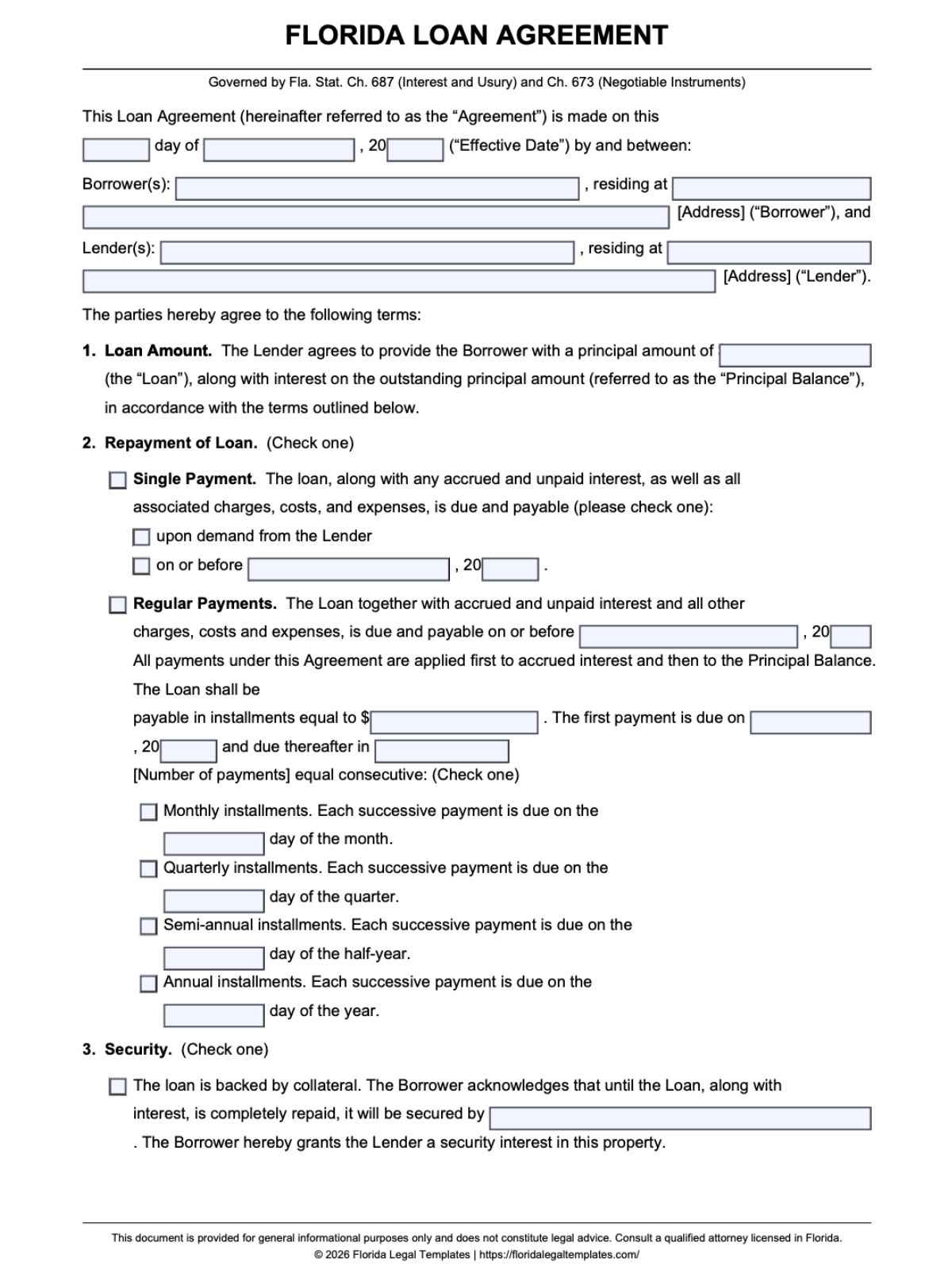

Florida Loan Agreement (PDF, Printable, Fillable)

A personal loan agreement Florida template provides a ready-to-use structure that includes the essential legal components required for enforceability.

What the document includes:

- Identification of lender and borrower

- Loan amount and disbursement terms

- Repayment structure (installments or lump sum)

- Interest rate and calculation method

- Default, late fees, and acceleration clause

- Governing law (Florida)

- Signature block

Who should use this:

- Individuals lending money privately

- Family or friend loan arrangements

- Small business or informal financing

- Peer-to-peer lending

When this template may NOT be sufficient:

- Loans secured by real estate (requires recorded mortgage)

- Loans secured by personal or business assets (requires UCC-1 filing)

- Institutional lending subject to federal regulations (such as TILA)

- High-value or structured commercial financing

A money lending agreement Florida is most effective when the loan is simple, unsecured, and clearly documented.

What Is a Florida Loan Agreement?

A Florida loan agreement is a contract where a borrower agrees to repay a lender under defined terms. It establishes legal obligations that can be enforced in court—if properly drafted.

Private lending arrangements often overlap with broader business or transactional relationships, especially when repayment is tied to services, investments, or asset transfers. In situations involving structured business obligations, parties may also rely on a separate purchase and payment agreement or formal business partnership structure to define rights beyond repayment alone.

Legal framework:

- Governed by Fla. Stat. Ch. 673 (Negotiable Instruments)

- Subject to Fla. Stat. Ch. 687 (Interest and Usury)

- Enforceability governed by Fla. Stat. Ch. 725

Legal nuance:

Not every loan agreement qualifies as a negotiable instrument. To meet that standard under Florida law, the document must contain:

- An unconditional promise to pay

- A fixed amount of money

- Payment on demand or at a definite time

- Payment to bearer or to order

These elements determine whether the debt can be transferred or sold.

If the agreement includes conditional language—such as repayment dependent on profits or future events—it may lose its status as a negotiable instrument under Fla. Stat. § 673.1041 and instead be treated as a standard contract, limiting its transferability.

Critical distinction:

- Loan Agreement: broader contract with detailed terms

- Promissory Note: simplified promise focused on repayment

Execution validity:

- No notarization required

- No witnesses required

- Must be signed to be enforceable

Key implication:

Under Florida law, oral loan agreements that extend beyond one year are not enforceable, making written documentation essential.

Key Florida Laws That Affect This Document

Summary of Applicable Laws

| Topic / Issue | Florida Legal Rule | Governing Statute |

|---|---|---|

| Statute of Limitations | 5 years to enforce written loan | Fla. Stat. § 95.11(2)(b) |

| Statute of Frauds | Must be written if repayment exceeds 1 year | Fla. Stat. § 725.01 |

| Age / Capacity | Must be 18 to enter binding contract | Fla. Stat. § 743.07 |

| Usury Limits | Loans ≤ $500k: >18% civil; Loans > $500k: >25% civil. Any loan > 25% is criminal usury. | Fla. Stat. § 687.02 & § 687.071 |

| Negotiable Instrument Rules | Must include unconditional promise to pay | Fla. Stat. § 673.1041 |

Florida courts closely examine repayment terms, fee structures, and default provisions when enforcing private lending agreements. Businesses lending money during ongoing service or consulting relationships may also benefit from written professional service terms to clearly separate compensation obligations from loan repayment obligations.

Practical Impact & Document Clauses

Florida’s lending laws directly shape how a Florida loan agreement must be written to remain enforceable.

Interest rates are strictly regulated. Florida imposes strict usury limits that vary based on the loan amount. For loans of $500,000 or less, charging more than 18% per year constitutes civil usury. For loans exceeding $500,000, the cap increases to 25% annually.

Any loan charging more than 25% interest is considered criminal usury under Fla. Stat. § 687.071, and rates exceeding 45% may result in enhanced felony penalties.

The consequences are significant. In civil usury cases, a lender may forfeit all interest and recover only the principal. In criminal cases, the lender may lose the entire debt, including the principal. See Fla. Stat. § 687.02.

In practice, for installment-based loans, the statute of limitations may apply separately to each missed payment. However, if the lender accelerates the loan after default, the limitation period typically begins for the entire balance at the time of acceleration.

This makes the interest clause one of the most critical parts of the agreement.

The repayment structure must be clearly defined. Without a specific timeline or demand provision, the agreement may fail to qualify as a negotiable instrument under Fla. Stat. § 673.1041, limiting transferability.

Under Fla. Stat. § 725.01, any loan extending beyond one year must be in writing and signed. Oral agreements in such cases cannot be enforced.

Florida imposes a documentary stamp tax on written loan agreements under Fla. Stat. § 201.08. The tax is calculated at $0.35 per $100 of the loan amount.

For unsecured loans, the tax is capped at a maximum of $2,450. However, if the loan is secured by real estate, no cap applies, and the full tax must be paid based on the total loan value.

A critical enforcement rule applies: a loan agreement cannot be enforced in a Florida court unless this tax has been paid.

In practical terms:

- Invalid interest terms can make the agreement illegal

- Missing written documentation can void enforceability

- Failure to pay required tax can block court enforcement

When to Use This Document

A Florida loan agreement should be used whenever money is being lent with an expectation of repayment.

Common use cases:

- Lending money privately

- Structuring personal or business loans

- Formalizing repayment obligations

Practical scenarios:

- Family or friend loans

- Startup or small business funding

- Informal lending arrangements

When NOT to use:

- Real estate-secured loans (require mortgage documentation)

- Asset-secured loans (require UCC filings)

- Regulated institutional lending

Using a written agreement ensures both parties understand their obligations and reduces the risk of disputes.

Written loan agreements are especially important when funding is provided informally between business owners, investors, or independent professionals. In consulting or startup environments where money is advanced before services are completed, parties often combine lending arrangements with separate project consulting terms to reduce disputes over repayment and deliverables.

How to Create or Fill Out the Florida Loan Agreement

Creating a loan agreement florida template involves more than filling in blanks—it requires legal precision.

Step-by-step process:

- Identify lender and borrower

- Include full legal names

- Specify loan amount

- Clearly state the principal amount

- Define repayment schedule

- Installments, due dates, or demand repayment

- Set interest rate

- Ensure compliance with Florida usury limits

- Include default and late payment terms

- Define penalties and consequences

- Add acceleration clause

- Allow full repayment upon default

- Confirm negotiable instrument elements (if applicable)

- Include unconditional promise and payment terms

- Execute agreement

- Both parties must sign

- Address documentary stamp tax obligations

- Ensure compliance before enforcement

- Store signed copies securely

If the loan involves business assets, transferred equipment, or installment-based purchases, the parties may also require separate written ownership transfer documentation to clearly establish what property, if any, is tied to the financing arrangement.

Practical tips:

- Always document loans exceeding one year

- Use clear and specific repayment terms

- Avoid ambiguous or excessive interest provisions

Although Florida law does not require notarization or witnesses, using a notary or self-proving affidavit can help prevent disputes over signatures and strengthen enforceability.

Limitations and Legal Considerations

A Florida loan agreement is subject to strict legal boundaries.

Key limitations:

- Cannot exceed statutory interest limits

- Cannot be enforced without paying documentary stamp tax

Florida-specific constraints:

- Must comply with usury laws under Fla. Stat. Ch. 687

- Must meet Statute of Frauds requirements

High-risk scenarios:

- Charging illegal interest rates

- Relying on oral agreements

- Ignoring tax obligations

Edge cases:

- Secured loans requiring additional filings

- Transferable debt instruments

- Loans involving minors (voidable contracts under Fla. Stat. § 743.07)

Understanding these limitations helps prevent invalid agreements and financial loss.

Attorney’s Fees Clause: Florida follows the “American Rule,” meaning each party pays their own legal fees unless the agreement states otherwise. Including a clause that awards attorney’s fees to the prevailing party can significantly improve a lender’s ability to recover costs in a dispute.

A loan agreement cannot grant unlimited authority over another person’s finances or legal affairs beyond repayment rights. Where broader financial authority is intended, parties may require a separate durable financial authorization form rather than relying solely on lending language.

Common Mistakes to Avoid

Charging interest above legal limits

Consequence: Contract becomes illegal and may lead to criminal liability.

Using oral agreements for long-term loans

Consequence: Agreement is unenforceable under Fla. Stat. § 725.01.

Failing to include repayment structure

Consequence: Disputes over timing and obligations.

Ignoring documentary stamp tax

Consequence: Court may refuse to enforce the agreement.

Confusing loan agreement with promissory note

Consequence: Missing required elements for enforceability or transferability.

Frequently Asked Questions (FAQ)

Is a Florida loan agreement valid without notarization?

Yes. Florida law does not require notarization for a loan agreement to be legally binding.

What is the maximum legal interest rate in Florida?

Under Fla. Stat. § 687.02, interest exceeding 18% may be civil usury, while rates above 25% may be criminal.

When must a loan agreement be in writing in Florida?

Under Fla. Stat. § 725.01, agreements exceeding one year must be written.

Can a loan be enforced without paying documentary stamp tax?

No. Under Fla. Stat. § 201.08, the loan cannot be enforced in court until the required tax is paid.

A properly drafted Florida loan agreement does more than record a transaction—it ensures legal enforceability, protects both parties, and prevents costly disputes under Florida law.