Florida Home Equity Agreement (Free PDF & WORD Template)

A Florida home equity agreement allows a homeowner to access the value built up in a property by using that equity as collateral for financing or an equity-sharing arrangement. Whether the transaction is structured as a traditional home equity loan, a revolving HELOC, or a modern equity-sharing arrangement, Florida law focuses less on the label and more on the substance of the transaction.

That distinction matters because, under Florida law, an agreement that secures repayment using real property equity is generally treated as a mortgage. As a result, homestead protections, spousal signature requirements, recording rules, foreclosure procedures, and lender compliance obligations can apply even when the parties believe they have created something different. A home equity agreement in Florida is often straightforward on paper, but small drafting or execution mistakes can make a lien unenforceable or prevent it from being properly recorded.

Candice Hayden, Legal Writer

Carly Johansson, Florida Contract Attorney

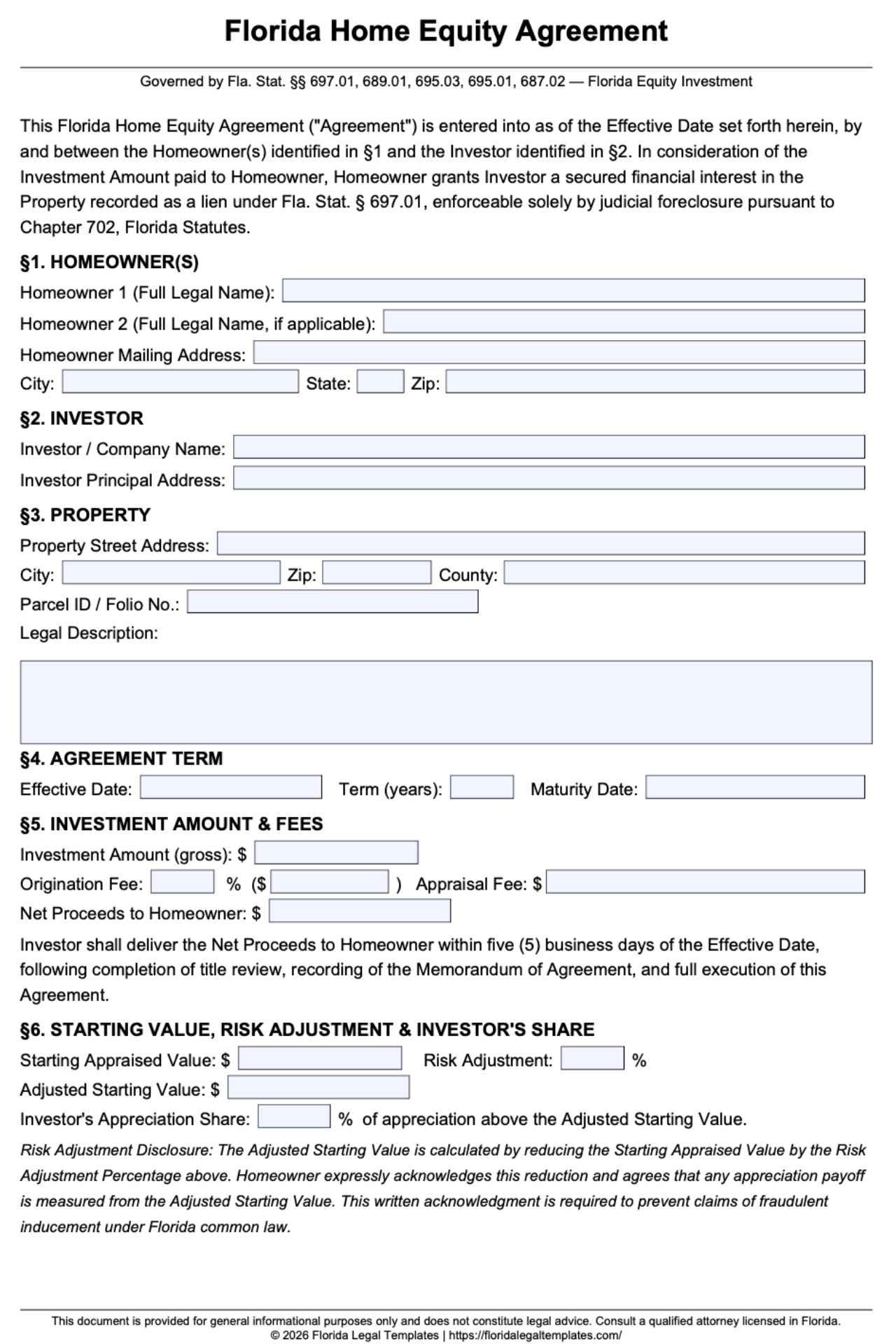

Free Florida Home Equity Agreement Template

A Florida Home Equity Agreement template typically includes:

- Legal names and addresses of all parties

- Property description

- Secured amount or maximum principal cap

- Lien-granting language

- Future-advances provisions (for HELOC-style arrangements)

- Borrower obligations and default terms

- Notary acknowledgment block

- Spousal joinder signature section where required

This type of template can be useful for:

- Private lenders

- Family and intrafamily loans

- Small investor-backed transactions

- Home Equity Investment (HEI) arrangements

- Homeowners reviewing lender-prepared documents

A template is not always enough. High-cost home equity loans subject to the Florida Fair Lending Act may require statutory disclosures and specific contract language. Institutional HELOCs frequently involve lender-specific compliance requirements. Likewise, a homestead property where a spouse refuses to sign creates a legal issue that no template can solve.

A common misconception is that signing the agreement creates a fully protected lien. In practice, the document only gains protection against third parties after proper notarization and recording in the county where the property is located.

What a Florida Home Equity Agreement Actually Is

A Florida home equity agreement generally falls into one of three categories:

- Home Equity Loan – a lump-sum loan secured by property equity.

- Home Equity Line of Credit (HELOC) – a revolving credit facility allowing future draws.

- Home Equity Investment (HEI) or Equity-Sharing Agreement – an arrangement where repayment may be tied to future property value appreciation.

The critical legal point is that Florida focuses on the function of the transaction rather than its marketing description. Under Chapter 697, an instrument securing money using real property equity is treated as a mortgage.

That means calling an agreement an “investment,” “equity participation,” or “shared appreciation arrangement” does not automatically avoid mortgage laws. If the transaction secures repayment using the property’s equity, mortgage rules can still apply.

Another distinction often overlooked is the difference between the debt and the security instrument. A promissory note creates the repayment obligation. The home equity agreement creates the lien against the property. One can exist without the other, but lenders usually require both.

Key Florida Laws That Affect This Document

Florida Statutory & Constitutional Matrix

| Topic / Issue | Florida Legal Rule | Governing Statute |

|---|---|---|

| Spousal Joinder on Homestead | Married owner’s spouse must join in mortgage of homestead property | Florida Constitution Art. X, § 4(c) |

| Notary Acknowledgment for Recording | Notarization required to record and perfect lien | Fla. Stat. § 695.03 |

| Future Advances Priority | Future advances retain priority if within 20 years and under stated cap | Fla. Stat. § 697.04(1)(b) & (2) |

| High-Cost Loan Rescission | Home equity loans and revolving HELOCs secured by a primary residence trigger an absolute, mandatory 3-business-day cooling-off period allowing unconditional cancellation. | Federal Truth in Lending Act (TILA), 15 U.S.C. § 1635; 12 C.F.R. § 1026.23 |

| Equity-Securing Instruments Deemed Mortgages | Security instruments using property equity are treated as mortgages | Fla. Stat. § 697.01(1) |

For statutory reference, see Fla. Stat. § 697.01, Fla. Stat. § 697.04, and Fla. Stat. § 695.03.

These rules affect enforceability far more than many borrowers realize. A lender may believe it holds valid collateral, only to discover years later that a missing spouse signature prevents foreclosure against a homestead property.

Likewise, future-advance provisions are not merely boilerplate. If the maximum principal amount is not properly stated, later draws may lose the priority protection that lenders typically expect.

Practical Impact & Which Clauses These Laws Dictate

The most significant clause for many Florida homeowners is the homestead spousal joinder requirement. Under Florida Constitution Article X, Section 4(c), a married homeowner generally cannot encumber homestead property without the spouse joining in the mortgage instrument.

Florida courts have reinforced the seriousness of this requirement. If a required spouse signature is missing, the lien may be ineffective from inception, preventing foreclosure until the defect is cured or homestead protections no longer apply.

The “deemed a mortgage” rule creates another practical consequence. Equity-sharing companies cannot bypass Florida mortgage law by calling themselves investors. If the agreement secures money using real estate equity, enforcement generally proceeds through judicial foreclosure rather than self-help remedies.

Future-advance clauses should clearly identify a maximum principal cap and comply with the 20-year priority framework established by Fla. Stat. § 697.04.

Mandatory Disclosures & Prohibited Terms for High-Cost Agreements

High-cost home equity transactions, equity-sharing options, and second mortgages are governed by the federal Home Ownership and Equity Protection Act (HOEPA) working alongside the Truth in Lending Act (TILA). Florida completely repealed the Florida Fair Lending Act (former Fla. Stat. §§ 494.0078–494.00797), shifting high-cost threshold enforcement entirely to federal compliance frameworks. Lenders originating high-cost equity-sharing or lending structures must deliver comprehensive Truth in Lending disclosures at least three business days before closing.

Under 12 C.F.R. § 1026.23, borrowers retain an absolute right to rescind a home equity contract until midnight of the third business day following closing, delivery of the rescission notice, or delivery of all material disclosures, whichever occurs last. If interest rates or commitment options remain subject to lender discretion prior to closing, mortgage lenders must comply with the separate state commitment disclosure rule under Fla. Stat. § 494.007(1)(c)2, printing the discretionary rate-setting warning in at least 10-point bold type.

Recording, Taxes & Perfecting the Lien

A signed agreement alone does not establish priority against competing claims.

To perfect the lien, the agreement must be recorded with the County Clerk of Court or Comptroller in the county where the property is located pursuant to Fla. Stat. § 695.01.

Recording generally requires a valid notarial acknowledgment under Fla. Stat. § 695.03.

Florida also imposes recording-related taxes that are often overlooked during private transactions:

- Documentary Stamp Tax: $0.35 per $100 (or fraction thereof) of maximum indebtedness secured

- Nonrecurring Intangible Tax: $2 per $1,000 of lien obligations

These taxes are not optional. The recording office may reject the filing if applicable taxes are not paid.

One drafting myth deserves special attention: witnesses are not generally required for validity or recording of a mortgage instrument under Florida case law. Many people focus on obtaining witnesses while accidentally overlooking notarization, which is the requirement that actually affects recording.

When This Agreement Is the Wrong Tool

A Florida home equity agreement works well when:

- Family members are documenting a secured loan

- A private lender is lending against equity

- An investor is structuring a compliant HEI transaction

- A borrower wants a recorded lien securing repayment

It may be the wrong document when:

- A required spouse refuses to join the mortgage

- An investor expects self-help eviction rights

- The parties are attempting to avoid mortgage taxes

- The transaction qualifies as a high-cost loan but compliance systems are not in place

Users also frequently confuse this agreement with:

- Promissory notes

- Satisfaction of mortgage forms

- Deeds in lieu of foreclosure

- Joint ownership agreements

- Equity-sharing ownership structures

Each serves a different legal purpose and carries different enforcement consequences.

How to Complete and Execute a Florida Home Equity Agreement

Step 1: Identify All Parties

List all owners, borrowers, lenders, and any spouse whose joinder may be required because homestead property is involved.

Step 2: Define the Secured Amount

Specify the secured obligation and any maximum principal cap. This affects both future-advance priority and tax calculations.

Step 3: Include Lien and Future-Advance Language

For revolving credit arrangements, clearly state future-advance rights and ensure the maximum principal amount is identified.

Step 4: Add High-Cost Compliance Language if Required

If the transaction falls within Florida’s high-cost lending framework, include all mandatory disclosures and prohibited-term compliance provisions.

Step 5: Obtain Spousal Joinder

If homestead property is involved and Florida law requires it, the spouse should sign the mortgage instrument itself.

Step 6: Execute Before a Notary

The acknowledgment or jurat must be properly completed to support recording.

Step 7: Pay Taxes and Record

Calculate documentary stamp tax and intangible tax before closing so sufficient funds are available. After execution, record the agreement in the county where the property is located.

Costly Mistakes Florida Borrowers and Lenders Make

Skipping spousal joinder on a homestead.

This can leave a lender with an unenforceable lien despite having a signed agreement and recorded document.

Calling the transaction an investment to avoid foreclosure laws.

Florida’s deemed-mortgage framework may still require judicial foreclosure.

Failing to pay recording taxes.

A rejected filing can allow intervening liens to gain priority.

Omitting the maximum principal cap.

Future advances may lose the benefit of original recording-date priority.

Missing high-cost disclosures.

This creates rescission risk and potential liability exposure.

Using witnesses but not a notary.

The document may be impossible to record even though everyone signed it.

Frequently Asked Questions

If my spouse isn’t on the deed and doesn’t live in the home, do they still have to sign?

For Florida homestead property, spousal joinder requirements can apply even when the spouse is not on the deed, is not a borrower, and resides elsewhere. The issue is homestead status, not merely title ownership.

Can a Home Equity Investment company evict me or take my house without going to court in Florida?

Generally, no. If the arrangement is deemed a mortgage under Florida law, enforcement proceeds through judicial foreclosure procedures rather than self-help eviction remedies.

How long do I have to back out after signing a high-cost home equity agreement?

For transactions covered by the Florida Fair Lending Act’s rescission provisions, borrowers have a 3-business-day right to rescind after closing or delivery of final disclosures.

Is my home equity agreement valid if it was notarized but had no witnesses?

Yes. Florida case law recognizes that witnesses are generally not required for validity or recording of a mortgage instrument. The critical recording formality is proper notarization under Fla. Stat. § 695.03.