Affidavit of No Florida Estate Tax Due [Free Printable, Fillable PDF]

The affidavit of no Florida estate tax due — commonly known as the DR-312 — is a form that Florida law no longer requires for most estates, yet it still shows up as a checklist item during property transfers because some title companies haven’t updated their procedures to reflect a change that took effect years ago.

Florida eliminated the DR-312 filing requirement under F.S. §198 for estates of decedents who died on or after January 1, 2005, a change confirmed in Florida Department of Revenue TIP #23C03-01, which means the florida affidavit of no estate tax due most title companies are still requesting has been officially retired by the state for essentially every estate being administered today. I’ve watched estate representatives spend weeks trying to obtain or file a form they didn’t need, delaying a property transfer that should have closed in days, simply because nobody questioned whether the title company’s checklist reflected current law.

The dr 312 affidavit florida information below explains what the form was, why it’s no longer required, and what to say when a title company asks for it anyway.

Candice Hayden, Legal Writer

Maria Rosso, Florida Probate, Guardianship and Estate Planning Attorney

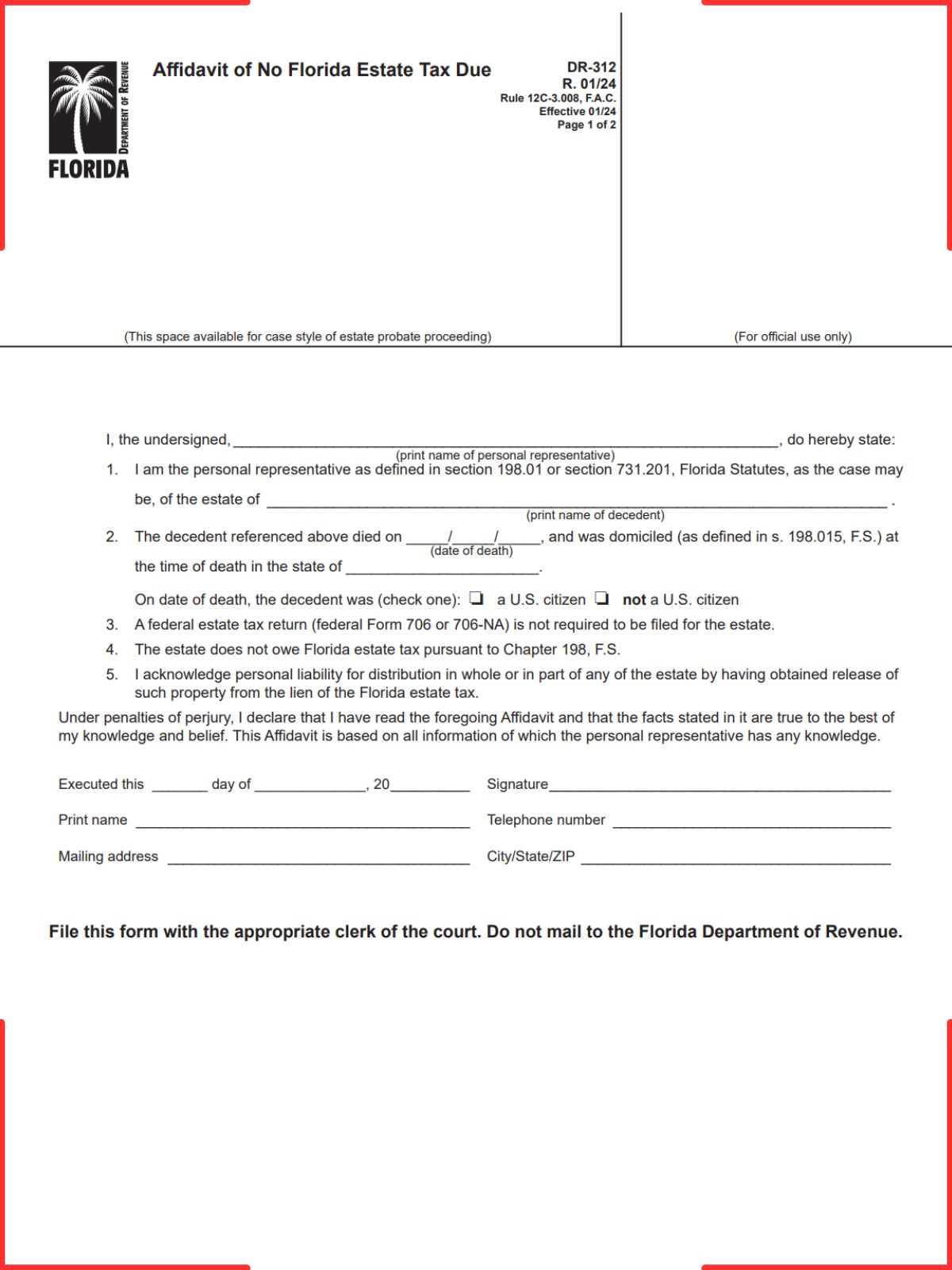

Affidavit of No Florida Estate Tax Due (Form DR-312 PDF, Printable, Fillable)

The Florida affidavit of no estate tax due (Form DR-312) is typically prepared as a fillable or printable document used in probate or real estate transactions.

What the document includes:

- Identification of the decedent (name and date of death)

- Identification of the affiant (personal representative or qualifying person)

- Statement that the estate is not subject to Florida estate tax

- Confirmation that no federal estate tax return (IRS Form 706) is required

- Mandatory acknowledgment of personal liability under Florida law

- Statutory perjury declaration (“magic words”)

- Notary jurat (sworn oath, not acknowledgment)

Who should use this:

- Personal representatives of estates

- Heirs or individuals in possession of estate property

- Anyone clearing title to Florida real estate

When this template may NOT be sufficient:

- The estate requires filing IRS Form 706 → you must use Form DR-313 instead

- Complex estates with possible tax exposure

- Ongoing probate disputes

- Multi-state estate issues

Key insight:This document is used to clear a lien on property—not to calculate or file taxes.

What Is an Affidavit of No Florida Estate Tax Due?

An affidavit of no Florida estate tax due is a sworn statement confirming that:

- No Florida estate tax is owed, and

- No federal estate tax return is required

Its primary function is to release the statutory lien placed on estate property.

Under Florida law, this process is governed by Fla. Stat. § 198.32.

Administrative procedures are further guided by Florida Administrative Code Rule 12C-3.0015.

Florida probate procedures involve several different sworn estate documents, readers handling inherited property may also benefit from reviewing other Florida affidavit forms commonly used in probate and title matters. In situations involving transfer of property after death without formal administration, a small estate transfer affidavit for simplified probate situations may also become relevant.

Legal nuance:

Florida’s estate tax system is tied to federal thresholds. This means:

- If no federal estate tax return is required → this affidavit can be used

- If a federal return is required → this affidavit is not allowed

Critical distinction:

- DR-312 affidavit Florida → No federal estate tax return required

- DR-313 affidavit → Federal return required but no Florida tax due

Key implication:

Using the wrong affidavit can delay or block real estate transactions because the lien will not be properly cleared.

Key Florida Laws That Affect Affidavit of No Florida Estate Tax Due

Summary of Applicable Laws

| Topic / Issue | Florida Legal Rule | Governing Statute |

|---|---|---|

| Use of Affidavit to Clear Lien | Removes estate tax lien if no tax/federal filing required | Fla. Stat. § 198.32(2) |

| Eligibility to Sign | Includes anyone in possession of estate property | Fla. Stat. § 198.01(2) |

| Notary Jurat Requirement | Must be sworn under oath (not acknowledgment) | Fla. Stat. § 117.05(13) |

| Perjury Declaration | Must include statutory perjury wording | Fla. Stat. § 92.525 |

| 2023 Update | Eliminated for New Probates. Effective July 1, 2023, the requirement to file DR-312 was technically abolished for all new probate proceedings. It remains “standard practice” only because title insurers still demand a recorded document to close the chain of title safely. | Fla. Stat. § 198.32(3); F.A.C. 12C-3.0015 |

The affidavit’s legal effect is closely tied to probate authority, title clearance, and the authority of the person signing on behalf of the estate. When estate representatives are managing broader legal or financial responsibilities, documents such as a Florida power of attorney for legal and financial authority are often reviewed alongside probate-related filings to confirm who can act in connected transactions.

Practical Impact & Document Clauses

The affidavit operates as a lien-release mechanism. Without it, inherited real estate may carry an unresolved tax lien, making it difficult—or impossible—to sell or refinance.

Florida law also expands who can sign the affidavit. Under Fla. Stat. § 198.01, the term “personal representative” includes any person in possession of estate property, such as an heir. This is broader than many users expect.

Two clauses are legally critical:

- Personal liability acknowledgment:

The affiant accepts liability under § 198.23. If taxes are later found to be due, the person signing the affidavit becomes personally responsible for the tax debt. - Perjury declaration:

The affidavit must include statutory language under Fla. Stat. § 92.525.

False statements constitute a third-degree felony.

Additionally, notarization must comply with Fla. Stat. § 117.05, which requires a jurat (oath)—not just a signature acknowledgment.

Real-world consequences:

- Missing clauses → document rejected

- Incorrect notarization → affidavit invalid

- False statements → criminal charges + financial liability

- Improper filing → lien remains on property

When to Use Affidavit of No Florida Estate Tax Due

You should use an affidavit of no Florida estate tax due when dealing with inherited property that needs to be transferred or sold.

Common use cases:

- Clearing estate tax lien from Florida real estate

- Preparing property for sale after death

- Completing probate-related real estate transactions

Practical scenarios:

- Heirs selling inherited property

- Title company requiring lien clearance

- Estate administration without federal tax filing

When NOT to use:

- Federal estate tax return is required

- Estate exceeds federal filing threshold

- Tax liability is uncertain

- Ongoing IRS or tax disputes

This affidavit most commonly appears during inherited property sales where title companies need confirmation that no Florida estate tax lien remains attached to the property. If the estate includes transferred vehicles or titled personal property, related ownership records such as a Florida vehicle transfer document may also need to match probate and title records before closing can proceed smoothly.

How to Create or Fill Out the Affidavit of No Florida Estate Tax Due

Preparing a DR-312 affidavit Florida requires careful attention to legal requirements.

Step-by-step process:

- Identify the decedent (name and date of death)

- Confirm no federal estate tax return (Form 706) is required

- Identify the affiant (qualified under Florida law)

- Declare that the estate is not subject to Florida estate tax

- Include the mandatory personal liability acknowledgment

- Insert the statutory perjury statement:

- “Under penalties of perjury…”

- Add a notary jurat (sworn oath required)

- Sign in the presence of a notary

- Record the affidavit with the Clerk of the Circuit Court in each county where property exists

- OR file it within the probate case if applicable

Practical tips:

- Confirm the estate is under the 2026 federal threshold of $15 million. If the gross estate exceeds this amount, you must file a federal return and use Form DR-313 instead.

- Use exact statutory wording—do not paraphrase

- Record the affidavit in every county where real property is located

Critical rule: Do NOT send this affidavit to the Florida Department of Revenue. It must be recorded locally to be effective.

Accuracy is critical when identifying heirs, estate property, and the person authorized to sign the affidavit. In probate situations where ownership rights or family succession are unclear, reviewing a Florida heirship declaration used to establish inheritance rights can help ensure the estate documentation remains consistent across filings and title records.

Limitations and Legal Considerations

This affidavit is limited in scope and should be used carefully.

Key limitations:

- It is not a tax return

- It cannot be used if federal estate tax applies

- It does not eliminate actual tax liability

Florida-specific constraints:

- Must include the personal liability acknowledgment

- Must comply with Fla. Stat. § 198.32

High-risk scenarios:

- Misrepresenting estate value

- Using DR-312 when DR-313 is required

- Failing to properly record the affidavit

Edge cases:

- Multi-county property ownership (requires multiple recordings)

- Joint tenancy property

- Estates near federal filing thresholds

This affidavit does not resolve disputes involving estate debts, financial disclosures, or contested liabilities between beneficiaries and creditors. In situations involving sworn financial disclosures during probate litigation or support proceedings, a Florida financial disclosure affidavit serves a separate legal purpose and follows different procedural requirements.

Common Mistakes to Avoid

Using DR-312 when federal return is required

Consequence: Invalid affidavit and delayed transaction

Missing personal liability clause

Consequence: Legal defect and possible rejection

Not including perjury statement

Consequence: Document may be unenforceable

Failing to notarize properly (no jurat)

Consequence: Affidavit invalid under Florida law

Filing with wrong authority

Consequence: No legal effect

Real consequences:

- Title defects

- Delayed real estate closings

- Personal financial liability

- Criminal penalties

Frequently Asked Questions (FAQ)

Do I need to file Form DR-312 with the Florida Department of Revenue?

No. The affidavit must be recorded with the county clerk or filed within probate—not sent to the Department of Revenue.

Who can sign an affidavit of no Florida estate tax due?

Under Fla. Stat. § 198.01, any person in possession of estate property—including heirs—may qualify to sign.

What happens if I sign DR-312 and taxes are later owed?

You may become personally liable for the tax debt, including repayment and penalties under Florida law.

Is this affidavit still required after the 2023 law changes?

Not always by statute. However, title companies still require it in most real estate transactions to ensure clear title.

A properly prepared affidavit of no Florida estate tax due is essential for clearing property title after death. Because it carries both financial and legal consequences, accuracy and compliance with Florida law are critical at every step.