Florida Personal Property Bill of Sale (PDF, Printable)

A Florida personal property bill of sale becomes important when privately buying or selling untitled items such as furniture, electronics, tools, collectibles, appliances, hobby equipment, or household goods. In many real-world transactions, the document functions as the only written proof showing who sold the property, who purchased it, what was transferred, how much was paid, and whether the item was sold “AS IS.”

That documentation matters far more once the transaction involves higher-value property. Under Florida law, contracts involving the sale of goods priced at $500 or more can become legally unenforceable without a written agreement signed by the party against whom enforcement is sought. Private sellers often discover this problem only after a payment dispute, ownership challenge, chargeback allegation, or damaged-property claim appears weeks later.

This bill of sale is different from bills of sale used for titled property such as motor vehicles, boats, or mobile homes. Those transactions carry separate Florida title-transfer laws, registration procedures, and statutory disclosure requirements that do not typically apply to ordinary untitled personal property.

Candice Hayden, Legal Writer

Carly Johansson, Florida Contract Attorney

Florida Personal Property Bill of Sale Template

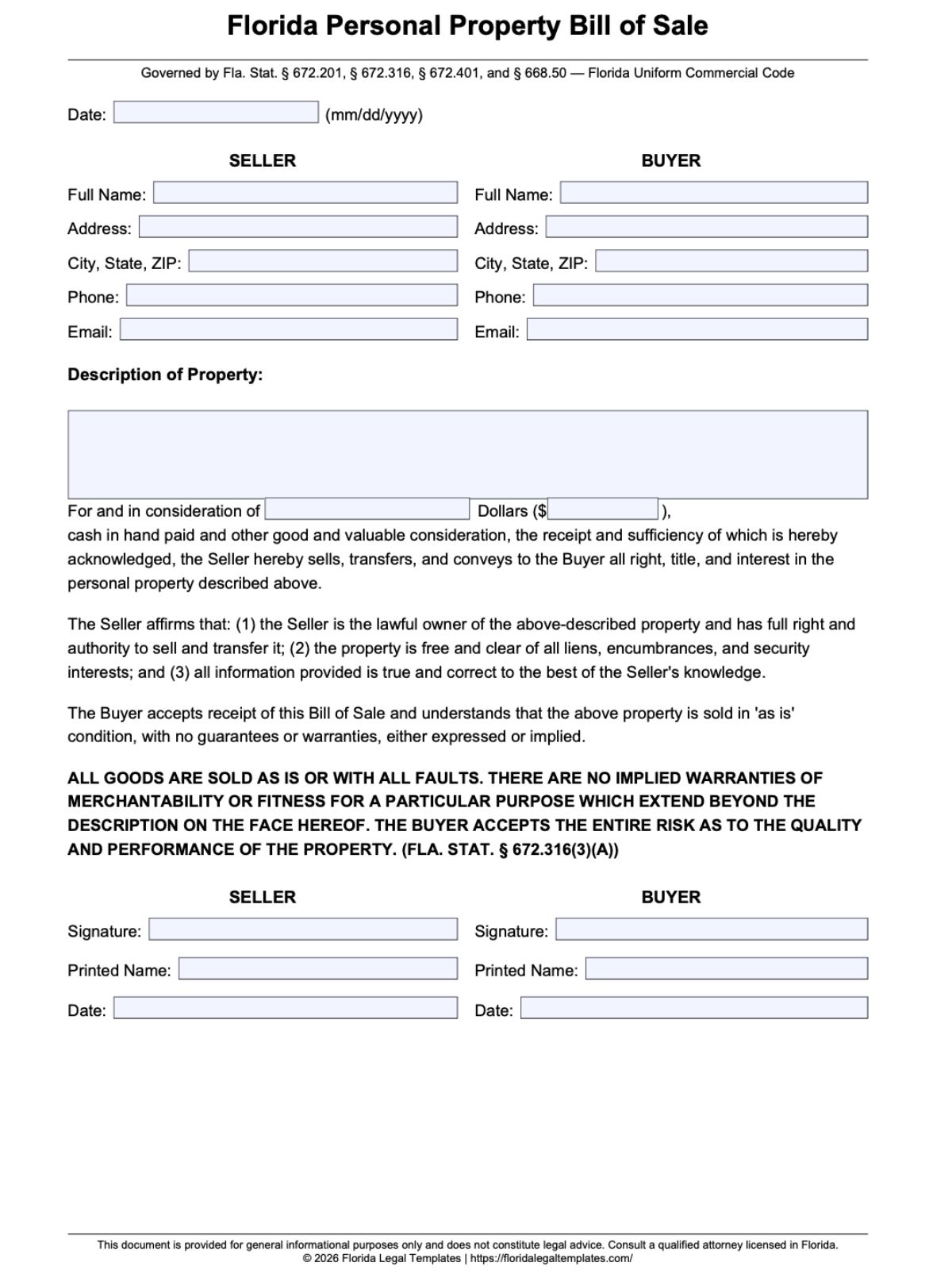

A Florida personal property bill of sale template is designed for private transfers of general tangible personal property between individuals. Most versions are available in printable and fillable PDF or Word formats for simple completion and recordkeeping.

Common uses include:

- Garage sale transactions

- Facebook Marketplace sales

- Furniture transfers

- Electronics sales

- Appliance sales

- Collectible transactions

- Household goods transfers

- Tool and hobby equipment sales

Most forms contain:

- Buyer and seller information

- Property descriptions

- Purchase price terms

- Delivery details

- Condition disclosures

- Warranty disclaimers

- Signature sections

A standard template may not adequately protect the parties when the transaction involves:

- Seller financing

- Installment payments

- Commercial inventory sales

- Titled vehicles or vessels

- Secured collateral

- High-value disputed assets

- Business asset transfers

Those situations often require additional agreements and security-interest language beyond a basic bill of sale, security-interest language, or Florida UCC filings.

What Makes a Florida Personal Property Bill of Sale Different From Other Bills of Sale?

This document exists primarily to prove the lawful transfer of untitled personal property in private transactions. Unlike a motor vehicle bill of sale or motor boat bill of sale, it is not normally tied to state title registration systems.

It also differs from:

- Commercial invoices used by retailers

- Business asset purchase agreements

- Firearm-specific transfer documents

- Consignment agreements

- Secured transaction paperwork

The legal focus here is narrower and more practical: documenting ownership transfer, payment terms, possession timing, and liability allocation between private parties.

Florida personal property sales are heavily influenced by Uniform Commercial Code sales law under Chapter 672. That creates issues many casual sellers overlook, especially involving:

- “AS IS” disclaimer language

- Oral agreement enforceability

- Risk-of-loss timing

- Warranty disputes

- Seller-financing problems

In practice, most users searching for this document are trying to create evidentiary protection before a dispute happens.

When a Florida Personal Property Bill of Sale Is Commonly Used

This form commonly appears in:

- Household property sales

- Craigslist or Marketplace transactions

-

Estate cleanouts and inherited property sales can create ownership disputes if authority to sell the property is unclear.”

- Downsizing sales

- Antique and collectible transactions

- Electronics transfers

- Tool sales

- Cash transactions between strangers

- Family property transfers

Many sellers also use the document specifically to include conspicuous ““AS IS” bill of sale language intended to reduce future complaints about condition or functionality.

The document should not be relied upon alone when the transaction involves:

- Titled property

- Commercial merchant inventory

- Seller-financed collateral

- Consignment arrangements

- Suspected stolen property

- Cross-state secured transactions

Key Florida Laws That Affect a Personal Property Bill of Sale

Florida Statutes That Directly Affect Private Personal Property Sales

| Topic / Issue | Florida Legal Rule | Governing Statute |

|---|---|---|

| Statute of Frauds | Sales over $500 generally require a signed writing for enforcement | Fla. Stat. § 672.201(1) |

| Warranty Disclaimers | “AS IS” and merchantability disclaimers must be conspicuous | Fla. Stat. § 672.316 |

| Risk of Loss | Private-sale risk can transfer upon tender of delivery | Fla. Stat. § 672.509(3) |

| Legal Capacity | Parties must generally be 18 and legally competent | Fla. Stat. § 743.07 |

| Seller Financing | Security interests may require UCC-1 filing | Fla. Stat. Chapter 679 |

| Contract Limitation Periods | Lawsuit periods cannot be extended beyond 4 years | Fla. Stat. § 672.725(1) |

| Unconscionability | Grossly unfair clauses may be limited or invalidated | Fla. Stat. § 672.302 |

| Casual Sale Tax Rules | Isolated private sales may qualify for exemption treatment | Fla. Stat. § 212.02(2) |

Florida’s sales laws become highly relevant once disputes arise. Many informal cash sales begin with trust-based verbal agreements but later collapse when parties disagree about condition, payment status, pickup timing, or ownership.

For example, sellers often assume typing “sold as seen” into a receipt automatically eliminates liability. Under Florida law, ineffective or hidden disclaimers may fail entirely if they are not conspicuous or properly drafted. Courts frequently examine whether the buyer had clear notice of the disclaimer before the transaction closed.

Review the state’s baseline rules via Fla. Stat. § 672.201(1)(Statute of Frauds), the Fla. Stat. § 672.316(Warranties), and Fla. Stat. § 672.509(3)(Risk of Loss). Financed options must be formally perfected through the Florida Secured Transaction Registry under Chapter 679.

How These Laws Affect Real Transactions

Oral agreements become particularly dangerous once property values exceed $500. A buyer may claim additional items were included. A seller may insist full payment was never received. Without written evidence, both parties face major evidentiary weaknesses.

Risk-of-loss rules also surprise many private sellers. Under Florida law, risk can transfer once the seller makes the property available for pickup and notifies the buyer. That means an item damaged after tender of delivery—but before actual pickup—can become a contested issue.

Seller-financed transactions create another common problem. A simple bill of sale rarely provides sufficient protection if the buyer defaults after taking possession. Without properly structured security-interest documentation and possible UCC filings, repossession rights can become legally difficult.

Clauses That Carry Special Legal Importance

The most important provisions usually include:

- Property identification language

- Purchase price terms

- Delivery and pickup timing

- “AS IS” disclaimer wording

- Payment acknowledgment

- Signature authentication

- Installment-payment terms

- Security-interest clauses

Each clause serves an operational purpose. Weak drafting frequently becomes the center of later disputes.

How to Properly Describe Personal Property in the Bill of Sale

Vague descriptions are one of the fastest ways to create ownership disputes.

Instead of writing:

“Used electronics”

A stronger description would identify:

- Brand

- Model number

- Serial number

- Quantity

- Cosmetic condition

- Included accessories

This becomes especially important for:

- Electronics

- Collectibles

- Tools

- Furniture

- Hobby equipment

- Bulk property sales

Photographs, receipts, and attached inventories can substantially strengthen evidentiary value. In estate cleanouts or moving sales, parties often later disagree about whether certain items were included. Detailed attachments reduce that risk.

Using “AS IS” Language Correctly in Florida

An “AS IS” clause is designed to limit implied warranties and shift quality-related risk toward the buyer.

Waivers must be visually conspicuous under Fla. Stat. § 671.201(2)(k) using bolding, distinct sizing, or all-caps. Under Fla. Stat. § 672.316, written disclaimers must explicitly state the word ‘merchantability’ or deploy direct phrasing like ‘AS IS’ or ‘WITH ALL FAULTS’ to fully cut off implied safety and functionality claims.

Florida also requires disclaimer language involving merchantability to specifically reference “merchantability” if that implied warranty is being excluded.

An “AS IS” clause does not protect sellers who intentionally conceal defects or commit fraud. A seller who knowingly lies about flood damage, stolen components, counterfeit collectibles, or major functional problems may still face legal exposure despite disclaimer language.

How to Create and Sign a Florida Personal Property Bill of Sale

A practical drafting workflow usually follows this order:

- Identify the buyer and seller

- Describe the property in detail

- State the purchase price

- Clarify payment timing

- Address pickup or delivery terms

- Add warranty or “AS IS” language

- Confirm possession transfer

- Sign and exchange copies

Florida does not generally require witnesses or notarization for a standard personal property bill of sale between private parties.

Still, notarization may help in situations involving:

- Fraud allegations

- Estate disputes

- Ownership challenges

- Higher-value property

- Cross-state enforcement concerns

Cash transactions between strangers should also document the exact payment date and amount received.

Risk of Loss Problems Buyers and Sellers Often Overlook

Many disputes occur after payment but before pickup.

For example:

- A garage roof leaks onto stored furniture

- An appliance is damaged during loading

- Electronics are stolen after payment but before collection

Florida’s “tender of delivery” rules can significantly affect who absorbs the financial loss.

Clear drafting helps reduce uncertainty. Strong agreements usually specify:

- Exact pickup deadlines

- Storage responsibility

- Transportation responsibility

- Possession-transfer timing

- Risk allocation after payment

Without those details, parties frequently argue over who became responsible for the property first.

Seller Financing and Installment Payment Risks

A standard bill of sale is often inadequate for financed transactions.

Once installment payments enter the picture, disputes commonly arise involving:

- Missed payments

- Repossession rights

- Ownership timing

- Damage before payoff

- Priority creditor claims

Sellers routinely assume they keep full title until final payment is clear. However, under Fla. Stat. § 672.401(1), any title retention upon delivery defaults down to a security interest. Retaining priority repossession rights against third parties requires a standalone Chapter 679 security agreement and a recorded UCC-1 filing.

That distinction becomes critical if the buyer later sells the property, files bankruptcy, or defaults.

Common Mistakes That Cause Disputes in Florida Personal Property Sales

Frequent problems include:

- Vague descriptions

- Missing signatures

- Undefined delivery terms

- Verbal side agreements

- Weak “AS IS” language

- Failure to document payment

- Using the wrong bill of sale form

- Confusing titled and untitled property

Generic online forms also create problems when they omit Florida-specific risk allocation or disclaimer language.

Financial consequences may include:

- Lost property claims

- Failed lawsuits

- Payment disputes

- Ownership litigation

- Inability to prove terms

- Unenforceable disclaimers

Situations Where a Personal Property Bill of Sale May Not Fully Protect You

Even a well-drafted document has limits.

Protection may weaken in cases involving:

- Fraud allegations

- Stolen property

- Intentional concealment

- Minor-capacity issues

- Unconscionable clauses

- Commercial merchant disputes

- Titled assets

- Cross-state transactions

Florida courts also retain authority under unconscionability principles to refuse enforcement of extremely unfair provisions.

Related Florida Documents Often Confused With This Form

Several related documents serve very different legal purposes:

- Vehicle bill of sale

- Boat bill of sale

- Firearm bill of sale

- Asset purchase agreement

- Security agreement

- Sales receipt

- Consignment agreement

A security agreement, for example, focuses on collateral rights after default. A vehicle bill of sale connects to title-transfer procedures. A sales receipt may only acknowledge payment without allocating legal risk.

Users frequently confuse these documents because they all involve property transfers, but their operational functions are different.

Frequently Asked Questions

Is a written personal property bill of sale required in Florida for items over $500?

Under Florida’s UCC statute of frauds, sales of goods priced at $500 or more generally require a signed writing to be enforceable against the party being sued. Fla. Stat. § 672.201(1)

Does an “AS IS” clause fully protect a Florida seller from future claims?

No. Fraud, intentional concealment, or ineffective disclaimer drafting can still create liability exposure.

Can a Florida personal property bill of sale be challenged in court?

Yes. Courts may examine capacity, forged signatures, unconscionability, unclear drafting, or fraudulent conduct.

Should a Florida personal property bill of sale be notarized?

Notarization is not generally required for validity, but it may strengthen evidentiary value in disputed transactions.

What happens if the property is damaged before the buyer picks it up?

That depends heavily on the delivery terms and Florida risk-of-loss rules under Fla. Stat. § 672.509(3).

Can this document be used for installment payments or seller financing?

It can document the sale, but financed transactions often require additional secured-transaction documents and possible UCC filings.

Final Review Checklist Before Signing

Before signing a Florida personal property bill of sale:

- Verify property descriptions

- Confirm payment terms

- Review “AS IS” wording

- Ensure signatures are complete

- Clarify possession-transfer timing

- Keep copies for both parties

- Attach supporting documents or photos

- Confirm the property is untitled and not separately regulated

Careful drafting at the beginning of the transaction is usually far less expensive than trying to reconstruct the agreement after a dispute develops.